![Comprehensive Guide to File Income Tax Return (ITR) in India [FY 2024-25]](https://wraptaxmedia.s3.amazonaws.com/blog_images/ITRForms.png)

Introduction

For the Financial Year 2024–25, the Income Tax Department has introduced New ITR Form formats, which differ significantly from those used in previous years.

Let’s break down the complexities of ITR filing.

Understanding the Basics: Types of Income and its Corresponding Forms

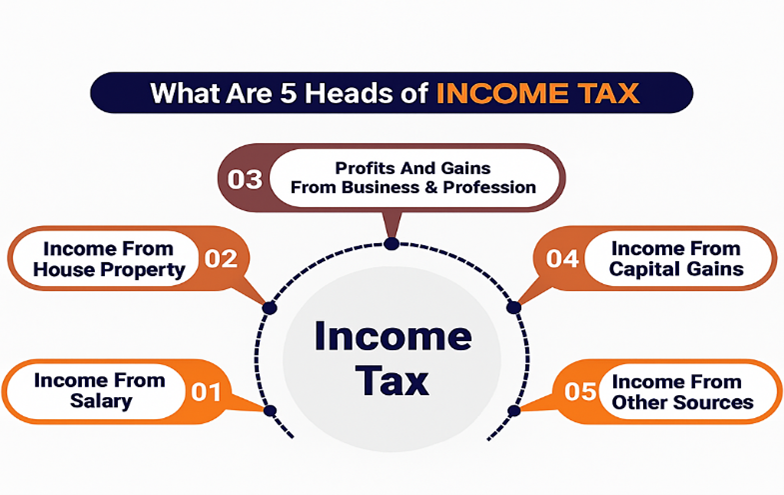

Heads of Income

There are five main Heads of Income which are defined by Income Tax Act, 1961:

- Salary

- Business/Profession Income

- Capital Gains (from sale of property, shares, etc)

- Income from House Property

- Other Sources (interest, lottery winnings, etc.)

The Type of Income you earn determines which ITR Form you should use. Here’s a breakdown:

ITR-1 (Sahaj)

Resident individuals (not HUF) with Total Income up to ₹50 lakhs from salary, one house property, and other sources such as interest income.

Not applicable if;

You have Income from Capital Gains, business or professional income, foreign assets or income, agricultural income above ₹5,000, or are a director in a company.

ITR-2

Applicable to Individuals and HUFs not having business or professional income. It covers income from salary, multiple house properties, capital gains, foreign income or assets, and dividend income.

Not applicable if;

You have income from business or profession, in that case, ITR-3 or ITR-4 would be appropriate.

ITR-3

Applicable to Individuals and HUFs having income from business or profession under a normal computation (not presumptive). This includes those maintaining books of accounts or earning income from speculative business, commissions, or intra-day trading.

ITR-4 (Sugam)

Specially designed for small businesses or professionals (consultants, doctors, advocates) who opt for **presumptive taxation under Section 44AD (business), Section 44ADA (professionals), or Section 44AE (transporters).

**Presumptive Limits

- Normal cases (where cash receipts exceed 5 percent of total receipts):

- Section 44AD: Up to ₹2 crore

- Section 44ADA: Up to ₹50 lakh

- Enhanced limits (where cash receipts do not exceed 5 percent):

- Section 44AD: Limit increased to ₹3 crore

- Section 44ADA: Limit increased to ₹75 lakh

These enhanced limits aims to promote digital payments while simplifying compliance for small taxpayers

Note: Filing the wrong form (for instance, ITR-1 instead of ITR-2) can result in a defective return notice from the tax department, prompting you to correct and re-file that.

Forms beyond ITR-4 (ITR-5, 6, 7) cater to companies, firms, and societies, which usually have dedicated tax professionals

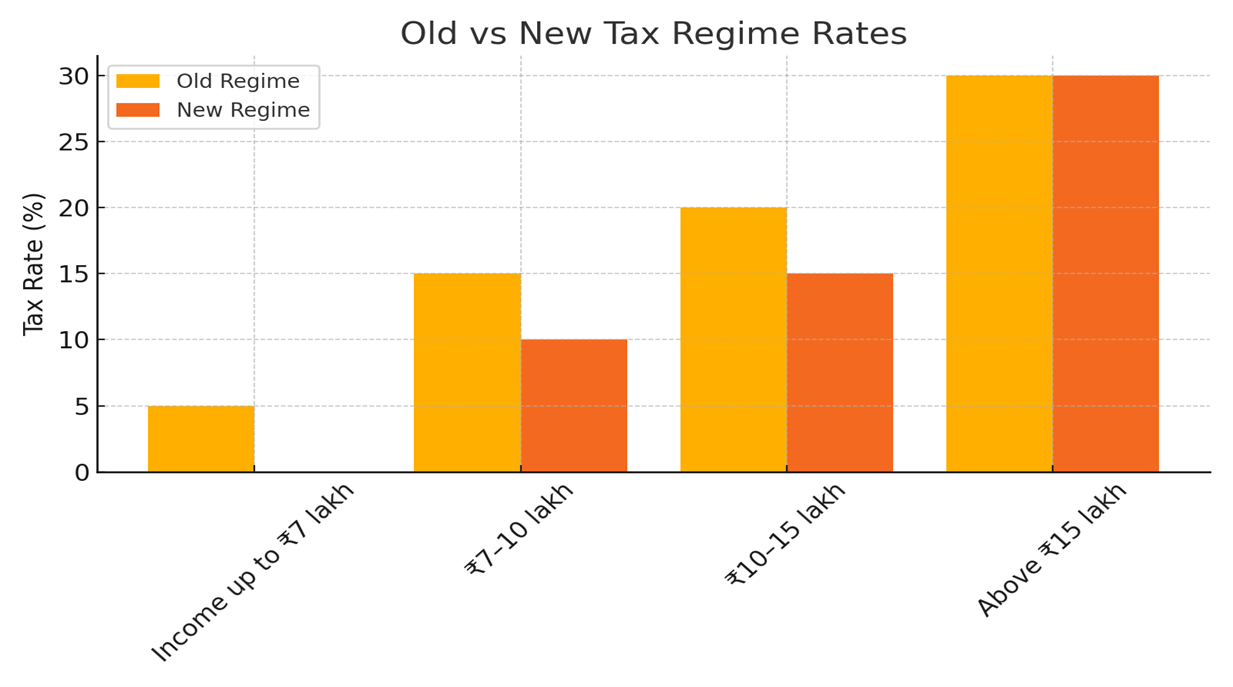

Choosing Between Old and New Tax Regimes

When filing, many taxpayers are unsure whether to opt for the old regime (with deductions) or the new regime (lower rates, fewer deductions). The choice depends on your specific financial situation and the deductions that are available. Avoid claiming false deductions to secure a refund, as the Income Tax Department has increasingly been issuing notices to taxpayers in recent years, asking for proof of the deductions claimed. It's advisable to carefully evaluate your eligible deductions before filing your return.

Note: The new regime offers lower tax rates but fewer deductions. Taxpayer should evaluate the beneficial regime before finalising the ITR.

Top 5 Common Mistakes to Avoid When Filing ITR

Following are the most frequent errors taxpayers make – and how to avoid them:

- Not Reconciling Form 26AS: Your Form 26AS summarizes TDS (tax deducted at source) and tax payments. Failing to reconcile it with your reported income can result in mismatch notices.

- Not Reporting High-Value Transactions: If you’ve made large purchases (like expensive jewellery) not supported by your declared income, the tax department might flag this as suspicious.

- Providing Incorrect or Incomplete Information: Errors or omissions can lead to notices or rejections.

- Claiming Unsupported Deductions: Common issues include claiming rent deductions without proof or other ineligible deductions.

- Failing to Report Foreign Assets: Even middle-income taxpayers increasingly invest abroad (e.g., shares, property in Dubai). Failing to declare these can result in notices.

Due date of Filing

The ITR filing deadline is July 31 but as per the CBDT Circular released on 27th May 2025 the due date of filing of ITRs are extended till 15th September 2025 (For individuals, HUFs, and other taxpayers not liable for audit). Don’t wait until the last minute – the portal might get congested, or you might face issues like power outages or system glitches.

The return filed during the filing year, may also called as Assessment Year, pertains to income earned during the last financial year (ending March 31). Only income up to this date counts for deductions and claims.