Form 15CA/15CB Filed — But Are You Really Compliant?

If you have recently filed Form 15CA or Form 15CB for a foreign remittance, it’s natural to feel relieved. But in cross border tax compliance, a “filed” status does not always mean compliant.

In 2025, the Income Tax Department and banks have significantly tightened scrutiny on 15CA/15CB filings. Even a minor error in Form 15CA CB filing can result in:

- Bank rejection of foreign remittance

- Tax notices

- Penalties up to ₹1,00,000 under Section 271I

Before moving ahead, review your Form 15CA and Form 15CB filing against these most common mistakes taxpayers make.

1. Incorrect Selection of Form 15CA Part

One of the most frequent 15CA filing mistakes is choosing the wrong part.

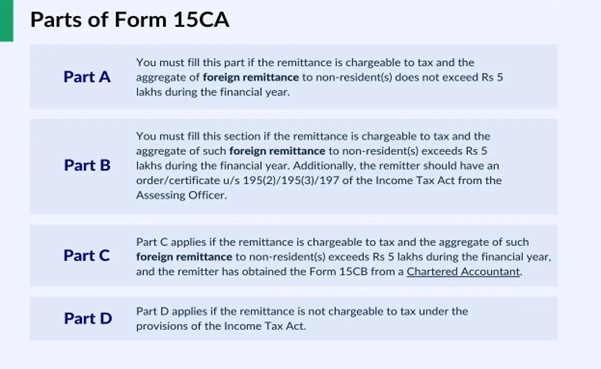

Form 15CA consists of four parts, and banks strictly validate this:

- Part A – Aggregate remittance below ₹5 lakh in a financial year

- Part B – Remittance backed by AO order/certificate u/s 195 or 197

- Part C – Taxable remittance exceeding ₹5 lakh (requires Form 15CB)

- Part D – Remittances not chargeable to tax under the Income Tax Act

Common mistake: Filing Part D for payments that are actually taxable (software fees, royalties, technical services).

Fix: Withdraw the incorrect Form 15CA and refile with the correct part selection.

2. Skipping Form 15CB for HighValue Taxable Payments

For taxable foreign remittances exceeding ₹5 lakh, Form 15CB from a Chartered Accountant is mandatory.

Common errors include:

- Filing 15CA Part C without a valid 15CB

- Repeatedly using Part A by splitting payments

Warning: Artificial splitting of remittances to avoid the ₹5 lakh threshold is a major red flag and can trigger audits.

3. Wrong Nature of Remittance Code in 15CA/15CB

The Nature of Remittance code is critical in 15CA/15CB compliance. It must align with:

- RBI purpose codes

- Income Tax Act provisions

- DTAA classification

Typical mistakes:

- Selecting Professional Services instead of Technical Services

- Using generic codes for royalty, commission or software payments

- Mismatch between agreement, invoice and remittance purpose

Fix: Cross verify the remittance nature with:

- Underlying agreement

- Invoice description

- RBI purpose code and DTAA position

4. Non Reporting of Grossed Up Payments

When the Indian payer bears the tax, the remittance becomes a grossed up payment.

Mistake: Reporting only the net amount in Form 15CA and Form 15CB.

Fix: Ensure gross up tax calculations are correctly reflected in both forms.

5. Ignoring Surcharge and Health & Education Cess

Many taxpayers apply only the base TDS rate while filing Form 15CA/15CB.

However, tax computation may also require:

- Surcharge

- Health & Education Cess

Fix: Recalculate tax considering surcharge and cess, unless DTAA benefit applies and cess is specifically excluded.

6. Missing or Invalid UDIN in Form 15CB

Every Form 15CB certificate must have a valid UDIN generated by the CA.

Common issues:

- UDIN not updated on the portal

- UDIN generated after the 15-day window

If invalid, the Form 15CB and related Form 15CA may be rejected.

Fix: Verify UDIN status under “View Filed Forms” on the income tax portal.

7. Mismatch in Remittee Details

Banks strictly verify foreign recipient details in 15CA/15CB filings.

Common causes of rejection:

- Spelling errors in remittee name or address

- Incorrect TIN or PAN (if available)

- Mismatch with bank portal or invoice

Fix: Ensure recipient details and RBI purpose code match across:

- Invoice

- Bank submission

- Form 15CA and Form 15CB

8. Ignoring DTAA Documentation (Form 10F & TRC)

To claim DTAA benefits and apply a lower tax rate:

- Tax Residency Certificate (TRC)

- Form 10F

are mandatory.

Mistake: Applying DTAA rates without a valid current year TRC.

Fix: Ensure the TRC corresponds to the relevant financial/calendar year of the recipient’s country.

How to Fix Errors After Filing Form 15CA/15CB

If you discover a mistake, act quickly:

- Withdraw Form 15CA within 7 days on the e-filing portal

- Revoke Form 15CB: CA must cancel the UDIN and certificate

- Fresh filing with corrected details

- Inform the bank with the new acknowledgment number

Timely correction avoids remittance delays and tax notices.

Why Correct 15CA/15CB Mistakes Immediately?

Ignoring errors in Form 15CA and Form 15CB filing can result in:

- Income tax notices

- Disallowance of expenses under Section 40(a)(i)

- Interest and penalties

- Future remittance and audit complications

Final Thoughts

Form 15CA/15CB filing is not a mere formality, it is a legal declaration of foreign remittance tax compliance.

A quick post filing review of your 15CA CB filing can save you from:

- Bank rejections

- Penalties

- Unnecessary scrutiny

If you have already filed, don’t assume it’s error free.

Review it now and fix issues while you still can.