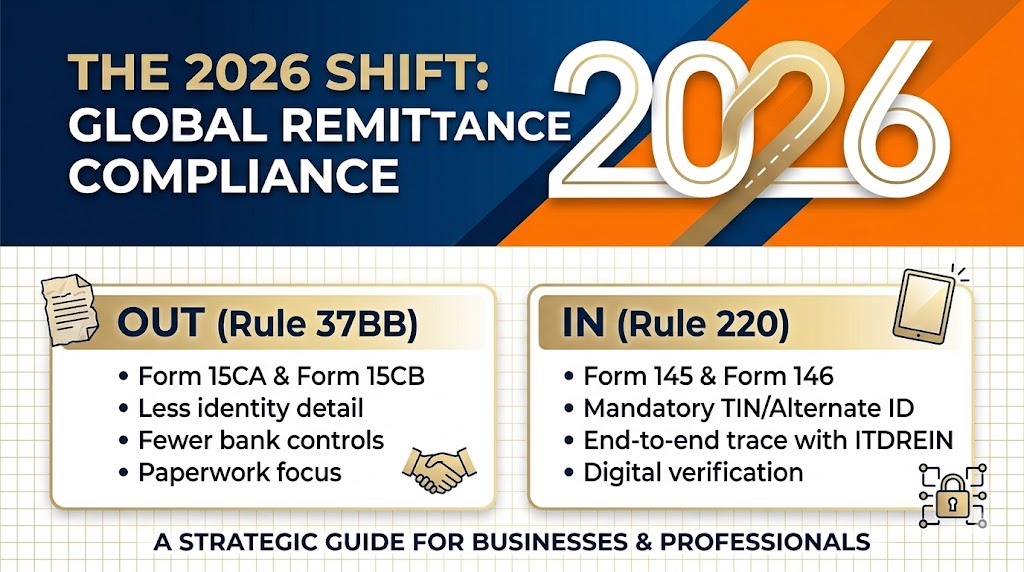

The Income-tax Rules, 2026 have introduced a completely revamped framework for reporting foreign remittances by replacing:

- Form 15CA / 15CB (Rule 37BB)

with - Form 145 / 146 (Rule 220)

This is not a mere procedural change—it represents a structural overhaul in reporting, documentation, and tax determination for cross-border payments.

1. Change in Legal Framework – Rule 37BB vs Rule 220

Under the new regime:

- Rule 220 governs furnishing of information for payments to non-residents

- It clearly categorizes compliance based on:

- Amount of remittance

- Taxability

- Nature of certification (AO / CA)

As per Rule 220: (Form 145 & 146)

- Part A: ≤ ₹5 lakh

- Part B: > ₹5 lakh with AO certificate

- Part C: > ₹5 lakh with CA certificate (CA Certificate in Form 146)

- Part D: Non-taxable remittances

While the broad classification of Parts (A to D) remains largely consistent with the earlier framework under Rule 37BB, the primary change lies in:

- Replacement of Form 15CA → Form 145

- Replacement of Form 15CB → Form 146

2. Significant Expansion in Remitter Details

Form 145/146 now requires comprehensive profiling of the remitter:

Newly Mandatory Fields:

- Residential Status (residential status as Resident, Non-resident, Resident but not ordinarily resident)

- Status (Individual, HUF, Company, Firm, AOP, etc.) - (Auto fatched from PAN)

- TAN (if available) - (Auto fatched from PAN)

- Email ID & Contact Number (Auto fatched from PAN)

These were not required in earlier Form 15CB, indicating a shift towards identity-based compliance tracking.

3. Strengthened Reporting for Remittee

The new rules significantly enhance global traceability.

Additional Requirements (Mandatory):

- Tax Identification Number (TIN) of country of residence

- Mandatory disclosure even via alternate unique ID if TIN unavailable

- Complete foreign address

- Email & contact details (If Available)

This aligns with international tax transparency standards.

4. Authorised Dealer & Banking Transparency

New disclosures include:

- Whether bank = authorised dealer

- If not, separate selection required

- Reporting of ITDREIN (Optional)

This ensures end-to-end traceability of remittance channels, which was missing earlier.

5. Explicit TDS Computation under the Act

A critical shift:

- Earlier (Form 15CB):

❌ No structured requirement to disclose tax rate under the Act (without DTAA) - Now:

✅ Mandatory reporting of:- Rate of TDS

This ensures that:

Tax under domestic law is determined first, before applying DTAA relief

6. Additional Details Required for DTAA Reporting

- In case of claiming DTAA benefit, it is mandatory to furnish:

- Tax Residency Certificate (TRC) Number

7. Pre-Filled Data & System Integration

The rules explicitly state:

- Certain fields will be auto-populated

This enhances:

- Accuracy

- Efficiency

- Reduced duplication

8. Form 146 (CA Certificate) – More Structured

Form 146 now requires:

- Separate section to report the UDIN (UDIN can be updated later)

9. Change in Verification Clause

There is a notable change in the verification/declaration section in Form 145/146 as compared to Form 15CA/15CB.

Key Enhancements:

- The verification is now more detailed and responsibility-driven

- It includes:

- Confirmation of correctness and completeness of information

- Acknowledgement of liability for short deduction or non-deduction of tax

- Acceptance of consequences including interest and penalties under the Act

This reflects a clear shift towards greater legal accountability of the remitter and certifying professional.

Conclusion

The transition from Form 15CA/15CB to Form 145/146 marks a fundamental shift in foreign remittance compliance.