Overview- Key Clarifications from the 47th GST Council Meeting

The 47th GST Council Meeting brought important clarity regarding the taxation of medical and allied services under GST. One of the major clarifications was that medical services provided by doctors in the field of Assisted Reproductive Technology (ART) and In Vitro Fertilisation (IVF) qualify as healthcare services and therefore continue to remain exempt from GST.

In addition, the GST Council reduced the tax rate on ostomy and orthopaedic appliances, including artificial implants, from 12% to 5%, making essential medical devices more affordable.

Another key update was that services provided by bio-medical waste treatment facility operators to hospitals and clinical establishments will now attract 12% GST, with the benefit of Input Tax Credit (ITC) available to the service provider.

In light of these developments, it becomes important to clearly understand how GST applies to dentists and dental clinics in India.

GST Applicability for Dentists in India

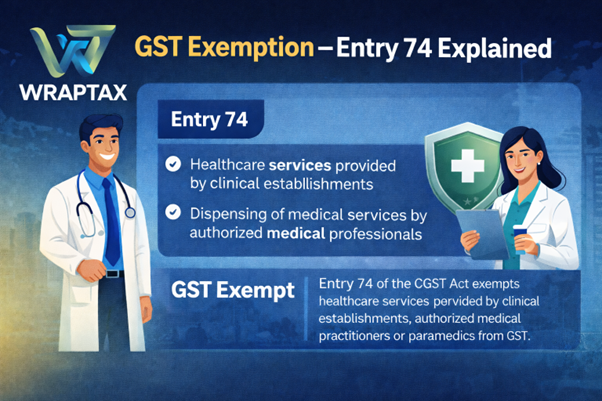

Dental services are treated as healthcare services under GST when they are provided for the diagnosis, treatment, or prevention of dental diseases or disorders. When such services are rendered by a registered dental practitioner or a recognised clinical establishment, they are fully exempt from GST.

However, cosmetic and aesthetic dental procedures that are not medically necessary do not qualify as healthcare services and are therefore taxable under GST.

Relevant SAC / HSN Codes

|

Activity / Service |

Applicable SAC |

Remarks |

|

Dental treatment services |

999312 |

Human health services – Exempt |

|

Cosmetic dental procedures |

999799 |

Aesthetic / non-medical services – Taxable |

|

Diagnostic / lab services |

999314 |

Exempt when linked to treatment |

|

Sale of medicines |

As per HSN |

Taxable as goods |

Legal Basis for GST Exemption on Healthcare Services

GST exemption for healthcare services is provided under:

- Notification No. 12/2017 – Central Tax (Rate)

- Notification No. 9/2017 – Integrated Tax (Rate)

These notifications were subsequently amended by Notification No. 04/2022 – CT (Rate) dated 13 July 2022, which refined the scope of exemptions and exclusions.

Scope and Limitations of Healthcare Exemption under GST

Services Eligible for GST Exemption

Healthcare services provided by the following entities are exempt:

- Clinical establishments

- Authorised medical practitioners

- Paramedical professionals

Services Not Covered Under Exemption

The exemption does not apply to:

- Room rent charged above ₹5,000 per day per patient, except for ICU, CCU and NICU rooms

- No Input Tax Credit is available on such taxable room rent

Services Excluded from the Definition of Healthcare

The following services are specifically excluded from the definition of healthcare services under GST:

- Hair transplant

- Cosmetic or plastic surgery

However, these services may still be treated as healthcare if they are performed for reconstruction or restoration due to:

- Congenital defects

- Injury or trauma

- Developmental abnormalities

In essence, healthcare services under GST strictly relate to the diagnosis, treatment, or management of disease, injury, deformity, abnormality or pregnancy.

GST Rate Chart for Dental Services

|

Nature of Supply |

GST Rate |

Notes |

|

Dental treatment, surgery, consultation |

Exempt (0%) |

Entry 74, Notification 12/2017 |

|

Cosmetic dental procedures (whitening, veneers, smile designing) |

18% |

Cosmetic in nature |

|

Sale of medicines |

5% / 18% |

Based on HSN |

|

Sale of implants / equipment |

18% |

Medical devices |

|

Consultancy to corporates |

18% |

Not healthcare services |

GST Exemption – Entry 74 Explained

Illustrative List of Exempt Dental Services

- Tooth extraction

- Root canal treatment

- Dental fillings and restorations

- Braces or aligners prescribed for medical reasons

- X-rays and diagnostic services directly linked to treatment

Illustrative List of Taxable Dental Services

- Teeth whitening for cosmetic enhancement

- Smile designing procedures

- Veneers used purely for aesthetics

- Sale of dental products

- Renting of clinic or commercial space

Input Tax Credit (ITC) Rules for Dentists

ITC Allowed (Only for Taxable Supplies)

- Dental chairs and medical equipment

- Medicines purchased for resale

- Clinic furniture and fittings

- Computers, software and IT systems

- Air conditioners and electrical installations

ITC Not Allowed

- Expenses exclusively related to exempt healthcare services

- Construction of clinic building (blocked under Section 17(5))

- Personal or non-business expenses

Special Rule – Mixed Supplies

If a dental clinic provides both exempt and taxable services, Rule 42 of the CGST Rules applies, requiring proportionate reversal of ITC.

Online Dental Consultancy to Foreign Patients

Where:

- The patient is located outside India, and

- Payment is received in foreign convertible currency,

Such services may qualify as an export of services and can be treated as zero rated supplies, subject to fulfilment of all statutory conditions.

GST Registration Requirements for Dentists

Dentists providing only exempt healthcare services are not required to obtain GST registration.

GST Registration Becomes Mandatory When:

- Cosmetic or aesthetic dental procedures are offered

- Clinic premises are rented out

- Online consultancy qualifies as export of service

- Corporate dental health contracts are undertaken

- Sale of medicines or equipment exceeds ₹20 lakh

- Inter-state taxable supplies are made

GST Compliance Requirements

Dentists registered under GST must:

- Issue tax invoices for taxable supplies

- Issue bills of supply for exempt services

- Maintain separate records for exempt and taxable income

- Apply Rule 42 wherever applicable

- File GSTR-1, GSTR-3B and GSTR-9 as applicable

- Discharge GST liability under Reverse Charge Mechanism (RCM) wherever required

Latest GST Updates for FY 2024–25

- No change in GST exemption for healthcare services

- Cosmetic and aesthetic procedures continue to attract GST

- Increased scrutiny on clinics selling medicines without charging GST

- Advance Ruling Authorities have reaffirmed exemption for genuine dental treatments

Practical Issues and Common Mistakes Observed

- Charging GST on exempt dental treatments

- Failing to levy GST on cosmetic procedures

- Incorrect usage of SAC or HSN codes

- Claiming full ITC despite providing exempt services

- Non-compliance with RCM provisions

- Issuing combined invoices for taxable and exempt supplies

Case Studies on GST for Dentists

Case 1: Tooth Extraction

- Nature: Healthcare service

- GST: Exempt

- Document: Bill of Supply

Case 2: Teeth Whitening

- Nature: Cosmetic procedure

- GST: 18%

- Document: Tax Invoice

Case 3: Mixed Services

- Root canal (exempt) and whitening (taxable) provided together

- Separate invoices required

- Proportionate ITC reversal applicable

Case 4: Online Consultancy to Foreign Patient

- Patient located outside India

- Payment received in foreign currency

- Eligible to be treated as export of service if conditions are met

Conclusion

GST applicability for dentists in India is entirely dependent on the nature of services provided. While medically necessary dental treatments continue to enjoy GST exemption, cosmetic and aesthetic dental services attract 18% GST. Accurate classification, correct invoicing and proper application of Input Tax Credit rules are essential to ensure compliance and avoid litigation. Seeking professional GST advisory support can help dental clinics remain compliant and penalty free.