“Impractical” Is Not a Defence: A Hard Lesson from ICAI’s Disciplinary Case (PR-117/2018)

Let’s be honest. Every auditor has faced this situation at least once — you’re auditing a company with hundreds (sometimes thousands) of debtors. The balances are material. You know SA 505 expects you to obtain direct confirmations. But practically? It feels impossible.

Emails bounce. Letters come back. Clients say they have a policy against sharing confirmations. And somewhere in the back of your mind, you think — internal ledgers are matching… maybe that’s enough.

The ICAI disciplinary case PR-117/2018 makes one thing absolutely clear: it’s not enough.

Where Things Went Wrong?

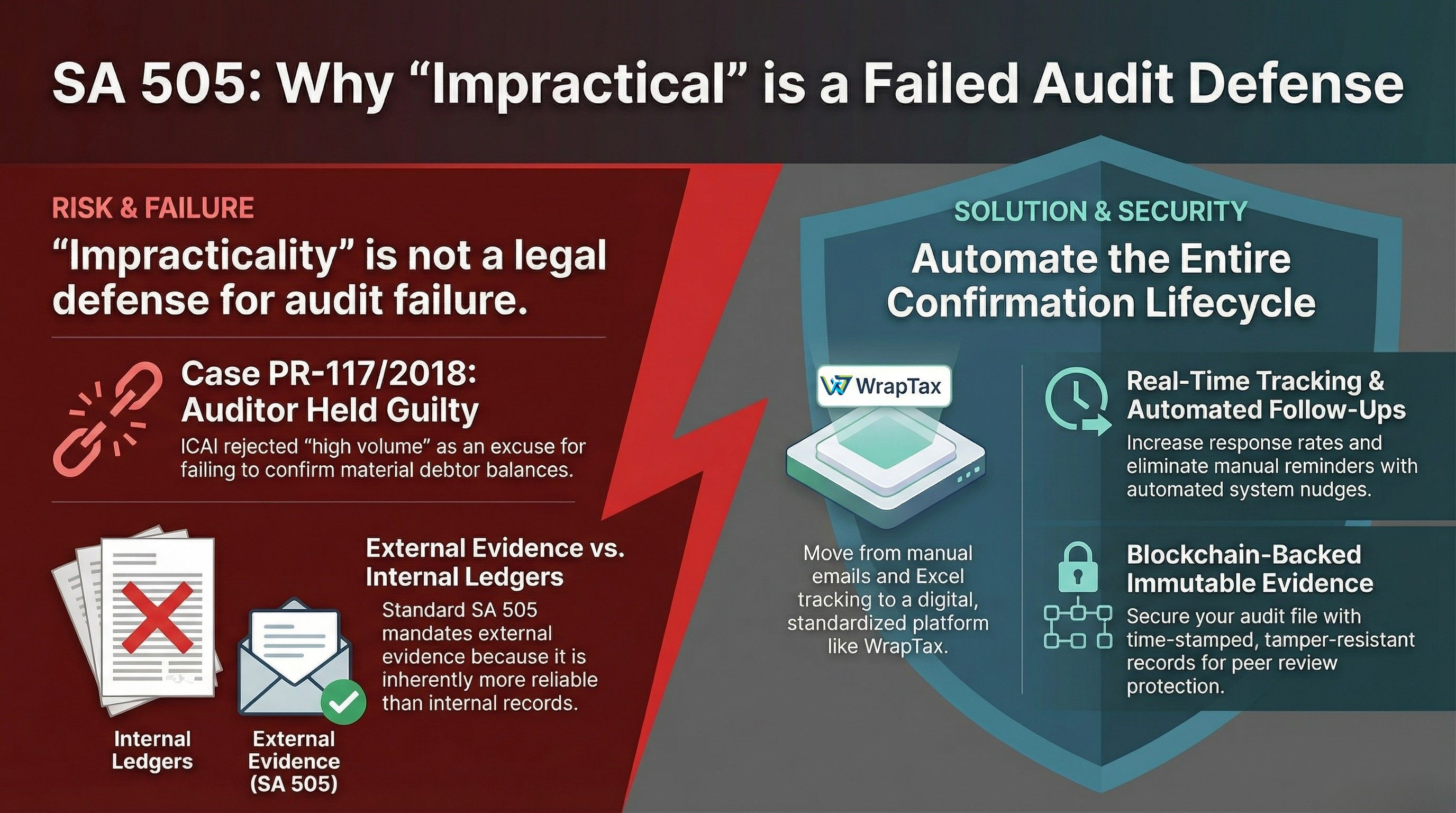

A statutory auditor failed to obtain external confirmations for material debtors (22% of the balance sheet). The defense was that the client’s policy did not permit it and the volume made it impractical. The Disciplinary Committee rejected this outright and held the auditor guilty of professional misconduct.

The message was simple —

If an item is material, you must obtain sufficient appropriate audit evidence. Practical difficulty is not an excuse.

Why This Matters

This case is not about one auditor. It reflects a common struggle — deadlines, resistance from clients, low response rates, and stretched teams. But standards are clear: external evidence is more reliable than internal records.

If balances are material, reliance only on internal ledgers is a professional risk.

The Real Issue: Process, Not Intent

The problem is logistical. Sending hundreds of emails manually, tracking responses in Excel, following up repeatedly — it’s exhausting. But responsibility does not reduce because the task is difficult.

The WrapTax Way: Turning Compliance Into Confidence

Let’s be practical. The problem isn’t that auditors don’t want to comply with SA 505. The real issue is the sheer operational burden of managing confirmations manually.

This is exactly where WrapTax changes the game.

Instead of sending scattered emails and tracking responses in Excel sheets, WrapTax digitizes the entire balance confirmation lifecycle:

- Digital Initiation: Send confirmation requests in a structured, standardized format directly from the platform.

- Automated Follow-Ups: No more manual reminders. The system automatically nudges non-responders at defined intervals.

- Real-Time Tracking Dashboard: See response status, pending confirmations, and exceptions in one place.

- Secure Documentation: Every communication is recorded and stored systematically.

- Blockchain Anchoring: Confirmation records are time-stamped and tamper-resistant, creating immutable audit evidence.

What does this mean for you as an auditor?

It means:

- Higher response rates

- Better documentation

- Reduced manual effort

- Stronger defensibility in peer review or disciplinary scrutiny

In today’s regulatory environment, documentation is not just compliance — it is protection.

Client policy will not save you.

Impracticality will not save you.

Volume will not save you.

But a structured, technology-backed confirmation process can.

When you adopt WrapTax, you’re not just automating a task — you’re strengthening your audit file. You’re building a clear trail of independent evidence. You’re showing that you exercised professional skepticism and due diligence.

And before signing any audit report, you can confidently ask yourself:

If this file goes before a disciplinary committee, am I comfortable defending my procedures?

With the right system in place, the answer becomes much easier.